Arizona’s Strong Recovery Remains Uneven

Second Quarter 2022 Forecast Update

May 2022

Arizona’s economy continues to recover unevenly from the pandemic. Jobs in three out of the state’s seven metropolitan areas were below their pre-pandemic level in April. Further, jobs in six out of 11 NAICS industries were below their February 2020 level as well. While statewide jobs have regained their pre-pandemic peak well before the U.S., they remain well below where they likely would have been had the pandemic not occurred. Overall, state and national labor markets remain in turmoil as employer efforts to rapidly ramp up production meet workers re-evaluating career objectives and opportunities.

The baseline forecasts for Arizona, Phoenix, and Tucson call for continued recovery from the economic impacts of the pandemic. Job growth remains strong this year, while income and sales growth rapidly decelerate, with the end of pandemic-related federal income support. Inflation is projected to remain very high this year before steeply decelerating in 2023. Downside risks to the baseline have increased in recent months, with large supply-side shocks and rapidly rising interest rates joining diminished federal income support to slow growth.

Arizona Recent Developments

Arizona seasonally-adjusted nonfarm payroll jobs increased by 16,100 in April, after a revised drop of 4,400 in April. The preliminary estimate for March showed a decline of 3,700 jobs.

Over-the-month job gains were driven by manufacturing, which added a whopping 4,900 jobs. That was followed by leisure and hospitality (up 4,600), education and health services (up 2,300), professional and business services (up 1,500), trade, transportation and utilities (up 1,200), information (up 1,000), other services (up 700), and government (up 500). Employment in natural resources and mining and financial activities was stable, while construction jobs dropped by 600.

The seasonally-adjusted manufacturing job gain in April was the largest on record (going back to 1966). Gains were about evenly split between durables (up 2,200) and nondurables (up 2,700). Durable job gains were concentrated in other durables (up 1,100), with additional gains in aerospace (up 500), computer and electronic products (up 400), and fabricated metals (up 300).

Arizona’s seasonally-adjusted unemployment rate dropped to 3.2% in April, down from 3.3% in March. The April estimate set another record low going back to 1976. (Exhibit 1).

Exhibit 1: Arizona and U.S. Unemployment Rates, Seasonally Adjusted

Government and leisure and hospitality jobs remained far below their pre-pandemic levels in April. Government jobs (primarily local government) were 20,300 below and leisure and hospitality jobs were 13,500 jobs below. Education and health services were still down 1,900, followed by information (down 1,200), natural resources and mining (down 200), and other services (down 100).

In contrast, trade, transportation, and utilities jobs were up 55,600 in April, followed by financial activities (up 11,200), manufacturing (up 10,600), construction (up 5,500), and professional and business services (up 3,000).

Overall, Arizona jobs were up 48,700 jobs from February 2020 to April 2022. Even so, state jobs were down 133,800 from where they would have been had the pandemic not occurred (Exhibit 2).

Exhibit 2: Arizona Jobs Are Far Below Their Pre-Pandemic Trend, Seasonally Adjusted, Thousands

There also remains a lot of variation in job recovery rates across Arizona’s metropolitan statistical area. The current estimates suggest that four of the state’s seven metropolitan areas have replaced all of the jobs lost during the February to April 2020 period: Lake Havasu City-Kingman, Phoenix, Prescott, and Yuma. As of April 2022, Sierra Vista-Douglas replaced 63.6% of the jobs lost early in the pandemic, Tucson replaced 88.4%, and Flagstaff replaced 92.2%. The U.S. rate was 94.6%.

Housing permit activity has been strong during the pandemic. At the same time, house prices continued to rise at a rapid pace. In April 2022, median house prices were up 24.8% over the year in Phoenix and 21.1% in Tucson. The Case-Shiller house price index, which measures repeat sales, was up 32.9% over the year in Phoenix in February, well above the national average increase of 19.8%. This has had a large negative impact on housing affordability in Arizona, particularly in the Phoenix MSA, where affordability has fallen well below the national average.

Labor compensation costs continued to accelerate in the first quarter of 2022, according to the BLS Employment Cost Index. The total compensation index (wages and salaries as well as fringe benefits) for the Phoenix MSA rose by 5.5% over the year in the first quarter of 2022. That was well above the national pace of 4.8% and faster than the 4.9% over the year increase to finish 2021. Even so, total compensation growth was well below the national rate of inflation in the first quarter, with the all-items consumer price index up 8.0% over the year.

Arizona Outlook

The outlook for Arizona, Phoenix, and Tucson depends in part on national and global economic events. The forecasts presented here are based on U.S. projections released by IHS Markit in April 2022. It was based on the following assumptions:

- During the spring of 2022, the winter wave of COVID (Omicron variant) fades and the transition from pandemic to endemic resumes.

- The forecast includes all of the pandemic relief enacted to date. The support to incomes from these measures, which averaged $2.7 trillion (annual rate) over the first half of 2021, dropped to less than $0.7 trillion by the fourth quarter. The forecast includes the Infrastructure Investment and Jobs Act and the recent Consolidated Appropriation Act of 2022 that funds government for this fiscal year. The forecast does not include the “Build Back Better” reconciliation bill.

- The Fed raises its policy rate six more times by late 2023, to a range of 3.0% - 3.25%. The Fed’s balance sheet declines by about one third through 2024.

- Tariffs and trade agreements between the U.S. and China since 2017 are assumed to continue.

- Real foreign GDP contracted by 4.7% in 2020. Growth rebounded to 5.6% in 2021 and then slows to 3.0% in 2022, amidst the fallout from the Russian invasion of Ukraine.

- The price of Brent crude oil is forecast to rise to $120 per barrel in the second quarter of 2022, up from $80 per barrel in the fourth quarter of 2021. The price then descends gradually back to $69 per barrel by mid-2026 due to demand destruction (caused by higher prices), a partial resolution of the conflict in Ukraine, and increased non-Russian production.

The baseline forecast (summarized here) is assigned a 50% probability. The pessimistic scenario is assigned 35% and the optimistic scenario is assigned the remaining 15%.

The baseline forecast calls for U.S. real GDP to rise by 3.0% in 2022 and then decelerate to 2.8% in 2023 and 2.7% in 2024. Compared to March, the April projections for real GDP were revised down in 2022, reflecting new data for the months preceding the Russian invasion of Ukraine that suggest slower growth in the first quarter.

Nonfarm payroll jobs nationally dropped by 5.8% in 2020 but rebounded in 2021 with growth of 2.8%. The forecast calls for jobs to rise by 4.0% in 2022 and 1.5% in 2023.

The unemployment rate peaked at 8.1% for the year in 2020 but fell to 5.4% in 2021. It is forecast to decline to 3.6% in 2022 and 2023.

Inflation gathered momentum last year, with an average annual price increase of 4.7%. The forecast calls for inflation to spike again in 2022 to 6.8%, reflecting the surge in oil prices this year. Inflation decelerates rapidly to 2.6% in 2023, as oil prices fall, supply-chain issues ease, and workers return to the labor force. With this forecast, inflation projections were raised by 0.6 percentage points in 2022.

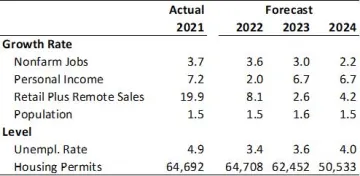

The national forecast sets the stage for continued growth in Arizona. Overall, Arizona jobs and population are forecast to grow at a solid pace in the near term, while income and sales growth decelerate with the end of federal income support. Exhibit 3 summarizes the Arizona forecast through 2024.

The revised employment data shows that Arizona added 105,200 jobs in 2021 (annual average basis using seasonally-adjusted data) for 3.7% growth. The baseline forecast calls for growth to decelerate slightly to 3.6% in 2022 and then to 3.0% in 2023.

The forecast calls for population growth to accelerate from 1.5% in 2022 to 1.6% in 2023, with the addition of 118,400 new residents by July 1, 2023. Most of that growth is driven by net migration.

Solid population gains contribute to housing permit activity continuing at a high level, with 64,708 permits in 2022 and 62,452 permits in 2023.

In contrast to solid job and population growth in 2022, personal income growth decelerates to 2.0% before adjustment for inflation and declines by 4.5% after adjustment for inflation, reflecting the end of federal income support related to the pandemic.

Retail sales (broadly defined to include food, retail, restaurants and base, and gasoline) growth decelerates to 1.9% in 2023 before adjustment for inflation and declines by 0.7% after adjustment for inflation. Taxable retail plus remote sales (narrowly defined) is forecast to decelerate from 19.9% growth in 2021 to 8.1% in 2022 and then to 2.6% in 2023.

Exhibit 3: Arizona Outlook Summary, Annual Growth Rates and Levels

VIEW MOST RECENT FORECAST DATA FOR ARIZONA, PHOENIX, AND TUCSON

If your business or organization requires more timely and in-depth forecast data and analysis, find out about the benefits of joining EBRC’s Forecasting Project and email EBRC director George Hammond at ghammond@arizona.edu.

Copyright 2022 Economic and Business Research Center, The University of Arizona, all rights reserved.